DATEV MITTELSTANDSINDEX

Subdued performance despite some modest momentum

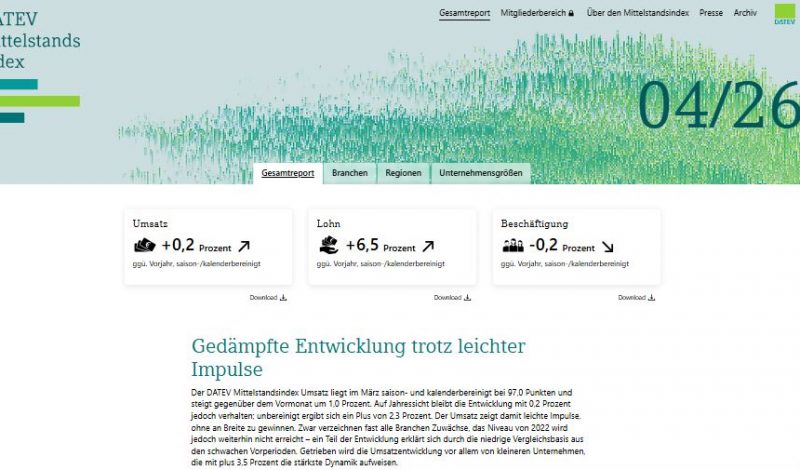

The DATEV SME Index for sales stood at 97.0 points in March on a seasonally and calendar-adjusted basis, up 1.0 percent from the previous month. However, year-over-year growth remains modest at 0.2 percent; on an unadjusted basis, the increase is 2.3 percent. Revenue is thus showing slight momentum without gaining breadth. Although nearly all sectors are recording growth, the 2022 level has still not been reached—part of this trend can be explained by the low base of comparison resulting from the weak preceding periods. Revenue growth is primarily driven by smaller companies, which, at 3.5 percent, are showing the strongest momentum.

The wage index continues its upward trend, though it remains firmly anchored on the cost side. Seasonally and calendar-adjusted, it rose to 124.4 points, up 0.5 percent from the previous month and 6.5 percent higher than a year ago. Wages are thus rising significantly across all sectors, particularly in the construction industry (7.9 percent) and among micro-enterprises (6.8 percent)—a trend that points more to persistent cost pressures than to economic strength.

Employment remained virtually unchanged in March. The seasonally and calendar-adjusted index stands at 100.9 points, representing a 0.2 percent decline compared with the previous year. While the manufacturing sector recorded the sharpest decline at 1.4 percent, and the hospitality and construction sectors also saw declines, the retail sector remained stable. At 0.8 percent, other services is the only sector above the previous year’s level. Among medium-sized enterprises, job losses accelerated to 0.8 percent.